The 30% Private Shift: Why HNW Investors are Exiting Public Markets for Asset Protection

Public markets are a glasshouse. In 2026, if you are a high-net-worth (HNW) entrepreneur with a standard brokerage account, you aren't just investing; you’re "displaying" your wealth for every predatory creditor and trial lawyer in the country.

The strategy that built your wealth, aggressive growth in public equities, is now the very thing that makes you a target. Most founders realize too late that an E-Trade or Fidelity account can be frozen or seized with a single court order in under 48 hours.

There is a structural migration happening right now. We call it the "30% Shift." Elite investors are moving nearly a third of their liquid net worth out of the "searchable" public domain and into the "opaque" world of Private Credit and Real Estate. They aren't just doing it for the 10% yields; they’re doing it because you can't seize what you can't easily find.

Why are investors moving 30% of their capital into private alternatives?

The 30% Shift is a strategic reallocation designed to achieve "uncorrelated alpha" while creating a structural barrier against litigation. By moving 30% of a portfolio into Private Credit and Real Estate, investors exit the high-visibility environment of public exchanges for private contracts that are significantly harder for creditors to discover or liquidate.

The Death of the 60/40 Portfolio

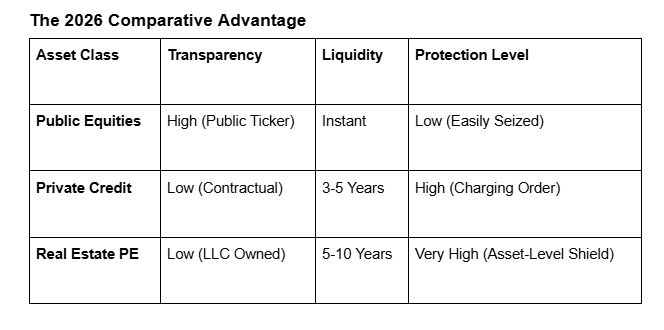

The traditional 60/40 split (stocks/bonds) is effectively dead for the HNW space. In 2026, volatility in public markets is no longer just a pricing risk; it’s a transparency risk. Public accounts are tied to your SSN or entity EIN in databases that any "asset hunter" with a $500 subscription can query.

Conversely, Private Credit, specifically senior secured lending, has become the preferred "safe haven." As highlighted on We Study Billionaires, institutional-grade private deals offer a yield premium that public bonds can't touch, often without the daily mark-to-market volatility that triggers margin calls or panic selling.

What makes Private Credit "lawsuit-opaque" compared to public equities?

Public brokerage accounts are held by centralized custodians who must comply with "Writs of Execution" immediately. Private alternatives are governed by subscription agreements and LLC structures. This creates a "seizure barrier" where a creditor cannot simply "take" the shares; they must navigate complex partnership laws that favor the existing members over outside interlopers.

A Tale of Two Seizures: The "Real-World" Reality

Imagine an entrepreneur, let’s call him David, who loses a high-stakes personal injury lawsuit stemming from a property he owns personally.

The Public Scenario: David has $1M in a standard brokerage account. Within 72 hours of the judgment, the creditor’s attorney serves the brokerage. The account is frozen. David’s liquidity vanishes instantly.

The Private Scenario: David has $1M split into a Private Equity Real Estate fund and a Private Credit vehicle. These assets do not show up on a standard bank sweep. Even if discovered, the creditor is met with a "Charging Order" protection.

In many jurisdictions, the creditor cannot force the fund to liquidate David’s position. They can only "charge" his interest, meaning if the fund pays a distribution, the creditor gets it. However, if the fund manager decides to reinvest that cash instead of distributing it, the creditor gets nothing, except, perhaps, a tax bill for "phantom income."

How do "charging orders" protect your Private Equity Real Estate investments?

A charging order is a court-authorized mechanism that allows a creditor to receive distributions from an LLC or partnership interest, but it does not grant them voting rights or the power to force a sale. In 2026, asset protection, this remains the "poison pill" that makes private assets unattractive to litigators seeking a quick settlement.

The "Apt Wealth" Strategy

According to the Apt Wealth Partners 2026 Asset Protection Guide, the goal of the 30% Shift is to make the "cost of collection" higher than the "value of the settlement."

When your wealth is tied up in private contracts:

Discovery is Difficult: There is no central registry for "Who owns 5% of this 200-unit apartment complex."

Valuation is Subjective: Unlike Apple stock, which has a ticker price, a private note’s value is based on the underlying contract, which may have "lock-up" periods of 5–7 years.

K-1 Complications: If a creditor successfully gets a charging order, they are technically stepping into the shoes of the partner for tax purposes. If the investment generates a K-1 with taxable income but no cash flow, the creditor is now paying taxes on money they haven't received.

Which private alternatives offer the best "make" and "protect" balance in 2026?

Investors are currently favoring Senior Secured Private Credit and Multi-family Real Estate syndications. These vehicles utilize "Non-Recourse Debt" at the asset level. This means if the project fails, the lender can only take the building. They cannot come after the individual investors, adding a final layer of separation between the investor’s personal estate and the investment risk.

Agentic Swarms and Due Diligence

In 2026, the barrier to entry for private deals has dropped thanks to "Agentic Swarms", AI-driven auditing tools. HNW investors are now using AI to scan 500-page Private Placement Memorandums (PPMs) in seconds to look for:

Specific Indemnification Clauses: Ensuring the investor is shielded from fund-level lawsuits.

Clawback Provisions: Protecting previously paid distributions.

Transfer Restrictions: Making the asset legally "un-transferable" to a creditor without manager approval.

What are the risks of the 30% Shift?

The primary risk is the "Liquidity Trap." While private assets are protected from creditors, they are also protected from you. If you need 50% of your net worth to bail out a primary business during a credit crunch, having 30% locked in a 7-year real estate fund could create a terminal cash flow gap.

The "30% Shift" isn't about hiding money. It's about changing the legal nature of your ownership.

Audit your "Seizure Velocity": How much of your net worth could a judge reach in 48 hours? If it’s more than 70%, you are over-exposed.

Diversify into Contracts, Not Tickers: Start by moving 10-15% into a Senior Secured Private Credit fund. This provides the "lawsuit-opaque" benefit while maintaining a predictable yield.

Update Your Entity Structure: Ensure your private investments are held within a properly structured holding company or a Bridge Trust as outlined in the Apt Wealth protocols.

In the 2026 legal climate, privacy is a luxury you have to buy. The 30% Shift is the price of admission for staying wealthy in an age of instant transparency.